You’re looking at a course page, a certification brochure, or maybe an application for a technical diploma, and your brain is doing two calculations at once.

First, the career one. Will this help you move into data, engineering, cyber, research, product, or leadership?

Second, the personal one. Can you afford it without making life harder for yourself or your family?

That tension is real. For many women in STEM, funding a qualification isn’t just about tuition. It sits alongside childcare, a career break, a confidence wobble after time away, or the need to catch up in a fast-moving field. If you’re mapping your next move, it helps to pair funding research with career research. A practical starting point is this guide to software developer careers, especially if you’re co...io/blog/software-developer-careers), especially if you’re comparing technical paths before paying for training.

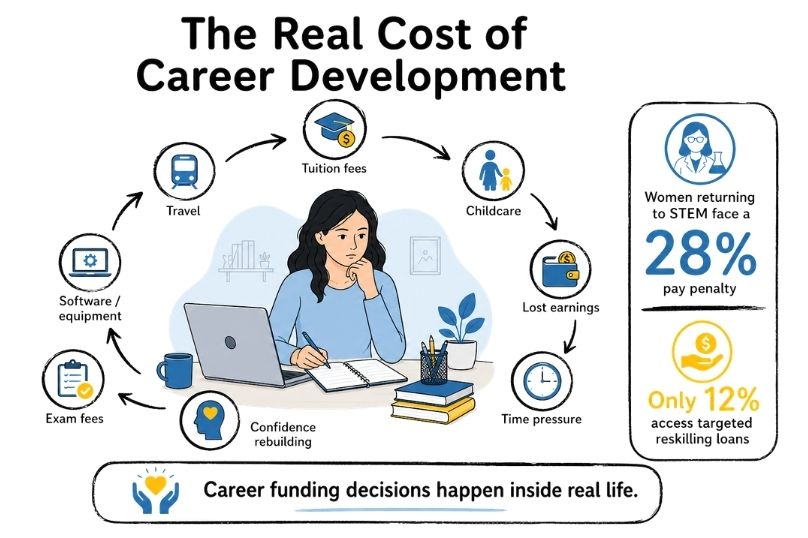

The stakes are not abstract. Women in STEM returning from career breaks face a 28% pay penalty, which can equate to a £126,000 lifetime earnings loss per woman, and only 12% of returners access targeted reskilling loans according to this NCDA-linked resource. That gap is about money, but it’s also about awareness.

Career development loans can still be a useful idea in 2026. The name often points people back to an older UK scheme that no longer operates in the same way, but the bigger concept remains relevant worldwide. Borrowing for career-focused training, then combining that with grants, employer support, and careful repayment planning.

If you’re actively exploring your next role, the Women in STEM jobs board for 2026 can also help you check whether the role you want values the qualification you’re considering. That small step matters. Funding works best when it supports a clear labour-market move, not a vague hope.

Your Next Step in STEM Starts Here

A lot of women arrive at this point after doing everything “right”. They worked hard, built solid technical skills, and kept going through changes at home and at work. Then the market shifted.

A new tool became standard. A management credential started appearing in job descriptions. A return to work after a break suddenly required fresh proof of current skills.

Why funding feels harder than it should

The problem usually isn’t just the price tag. It’s uncertainty.

You might be asking:

Will this qualification lead to work: especially if you’re re-entering STEM after time away.

Should I borrow or wait: because a grant or employer-funded option may exist, but isn’t always easy to find.

What if I finish the course and still need time: to secure the right role.

Those questions are sensible. They don’t mean you lack confidence. They mean you understand that debt and career choices are connected.

Borrowing for training should support a specific career move, not compensate for a lack of career direction.

What career development loans really mean now

In plain language, career development loans are loans used to pay for work-focused learning. That may include a technical certification, a diploma, a postgraduate vocational course, or leadership training that helps you move into a more senior role.

In some countries, these are formal government-backed products. In others, they’re private education loans, skills loans, or professional development finance. The labels vary. The core decision doesn’t.

You’re weighing today’s cost against future opportunity.

That’s especially relevant in STEM, where training often has a direct connection to employability. The challenge is that women don’t always enter this decision from the same starting point as men. Career breaks, uneven progression, and caregiving costs change what “affordable” means in practice.

A better way to approach the decision

Start with the role, then the course, then the funding.

That order helps you avoid paying for credentials that sound impressive but don’t strengthen your actual position in the jobs market. If you can say, “This course helps me return to engineering”, or “This qualification supports a move from analyst to team lead”, then you’re already making a stronger funding decision.

The rest of this guide focuses on the UK because the old Professional and Career Development Loan system created so much confusion. But the underlying lessons apply more widely. Understand the loan. Compare it with non-loan support. Budget for real life, not ideal life. Then borrow only what serves your next step.

The Legacy of UK Professional and Career Development Loans

You find a course that could help you return to software engineering after time out for caregiving. The syllabus fits the roles you want. Then your search leads you into old UK guidance on Professional and Career Development Loans, and suddenly it looks like there used to be one clear funding route that no longer exists.

That confusion is common, especially for women in STEM who are comparing retraining, returnships, leadership programmes, and technical certifications while also balancing childcare, part-time income, or a career break penalty. PCDLs matter now because they shaped how people in the UK still talk about “career development loans,” even though the scheme belongs to an earlier funding system.

How the old UK scheme worked

The former UK PCDL scheme was built for job-focused learning. Eligible borrowers could apply for up to £10,000 for approved training, and the provider had to be part of the scheme. Courses could run for up to two years, or three years if they included a year of unpaid practical work experience. The loan could cover tuition and, within the overall cap, some related costs such as travel, childcare, or living expenses. Borrowers had to be adult UK residents, and the training had to support employability rather than a first degree or foundation course, as outlined in this Cedefop summary of the UK scheme.

That made PCDLs narrower than many people assume. They sat between a student loan and a personal loan. The purpose was specific. Pay for training that could improve your position at work.

For women in technical fields, that design still feels familiar. A returner updating cloud credentials, a laboratory scientist adding regulatory training, and an engineer preparing for first-line management all face the same basic question. Is the course tightly linked to a real next role, or does it just sound impressive?

Why the scheme felt different for different applicants

The hardest part to understand was not the headline amount. It was the way support changed depending on your circumstances before the course began.

Under the old rules, some borrowers received more help with interest during study than others. In practice, employment status affected short-term affordability. Two applicants taking similar training could face very different costs at the point when cash flow was already tight.

That matters for a 2026 reader because women returning to STEM often deal with uneven income in exactly that early period. You may be paying for childcare before your salary recovers. You may be rebuilding confidence, contacts, and recent experience at the same time. A funding option that looks manageable on paper can feel very different if your household budget has little margin.

What the legacy still teaches us about borrowing

PCDLs also left behind a useful lesson about repayment. Interest support during study can soften the first stage, but it does not erase the cost of debt once repayments start.

That is why the old scheme works best as a reference point, not as a model to copy. It reminds you to look past the reassuring headline. Ask what happens after the course ends, when you are still waiting for the promotion, the first contract, or the return-to-work role.

A good funding decision works like a lab test. You do not judge it by one reading. You check several conditions before you trust the result.

Why this still matters in 2026

PCDLs are no longer the answer for new applicants, but they still help explain the current UK funding puzzle. Many women search for one central scheme because that used to be the frame. In 2026, the stronger approach is usually to build a package instead: one part loan alternative, one part employer support, and, where possible, one part grant funding.

That shift matters even more for career returners and mid-career leaders in STEM. If you are stepping back in after time away, borrowing the full cost yourself can increase the financial penalty of that break. If you are aiming for leadership, employer sponsorship may be more realistic than a retail-style loan because your training has a clearer business case.

So use the old PCDL model as a checklist, not a destination. Ask:

What costs are covered

When interest or fees begin

Whether the provider is eligible under the funding route

What happens if your income is irregular after training

How much you will repay in total

Which parts could be covered by your employer or a specialist grant

For some readers, that final point opens better options than a loan alone. If your course supports entrepreneurship, consultancy, or a return to technical self-employment, it is also worth reviewing women’s grants for business in the UK alongside training finance.

The old scheme treated employability-focused learning as an investment worth funding. That idea still holds. The difference now is that women in STEM often need a more flexible plan, one that reflects career breaks, promotion gaps, and the cost of rebuilding momentum.

Your 2026 UK Funding Options for Career Growth

The UK no longer offers one simple replacement for the old PCDL model. What exists instead is a patchwork. Some routes are formal. Some are negotiated. Some are easy to miss if you only search for “loan”.

For most women in STEM, the strongest approach is usually layered. Start with support you don’t repay. Add employer help if available. Use borrowing only for the remaining gap.

The main funding routes to compare

Here’s a practical view of the options many women now assess.

UK Career Development Funding Comparison (2026)

Best For

Typical Amount

Interest Rate

Key Consideration

Advanced Learner Loans

Eligible formal study in approved settings

Varies by course and provider

Depends on current loan rules

Best for approved courses, not every STEM upskilling route

Private career loans

Short vocational or professional courses

Varies by lender

Varies by lender

Check total repayable, not just the headline monthly payment

Employer sponsorship or reimbursement

Job-relevant training with a clear business case

Varies by employer policy

Not applicable if fully funded by employer

May come with grade, tenure, or clawback conditions

Specialist grants or scholarships

Women in STEM, returners, or leadership development

Varies by scheme

Not applicable if grant-based

Often competitive, narrow in scope, and deadline-sensitive

Blended funding

Courses that need multiple sources

Varies

Mixed

Works well when no single source covers fees plus life costs

The table doesn’t name exact amounts for current alternatives unless a verified figure exists. That’s deliberate. In this part of the market, terms change often and vary sharply by provider.

When an employer should be your first call

Many women look at loans before speaking to their employer. That’s often the wrong order.

If your course supports a current role or a near-term progression path, ask HR or your manager whether they offer:

Tuition reimbursement: where you pay first and claim back later.

Direct payment: where the employer pays the provider.

Study leave or protected learning time: valuable if time, not just money, is the barrier.

Partial sponsorship: where they fund one module, exam, or certification stage.

This route is especially strong for technical certifications, compliance-heavy roles, and leadership programmes linked to promotion planning.

Grants and specialist support can reduce borrowing

A loan doesn’t have to carry the whole cost.

That’s where focused grants and niche awards matter. If your training sits near entrepreneurship, innovation, or professional development, it’s worth reviewing opportunities such as this collection of women’s grants for business in the UK. Even if a grant doesn’t cover tuition directly, it may free up your own cash for fees, software, travel, or childcare.

Practical rule: if you can replace even part of a loan with grant funding or employer support, you reduce both repayment pressure and career risk.

Private loans need sharper scrutiny

Private career development loans may be appropriate when your course is clearly employability-focused and no grant or employer option is enough.

But women often need to slow down and read the detail. Ask:

Is the rate fixed or variable

When do repayments begin

Can you make overpayments without penalty

Does the lender pay the provider directly

What happens if the course is delayed or interrupted

A lender may market flexibility, but what matters is how that flexibility works under stress.

Blended funding often works best for returners

A returner to STEM may need more than tuition support. You may also need updated equipment, transport, childcare cover, or a buffer while rebuilding professional momentum.

That’s why a blended plan can be more realistic than a single large loan. For example:

use savings for the deposit or first module

apply for a specialist grant

request employer support if you’re already back in part-time or contract work

borrow only for the final shortfall

This approach takes more admin. It often creates a more manageable outcome.

A simple filter for choosing between options

If you feel stuck, judge each option on five things:

Fit: does it cover your actual course type

Speed: can you secure it before enrolment deadlines

Cost: what will repayment look like in real life

Risk: what happens if work doesn’t follow immediately

Control: can you change pace, repay early, or pause if needed

The right funding path isn’t always the biggest one or the fastest one. It’s the one that gives you training without trapping your future choices.

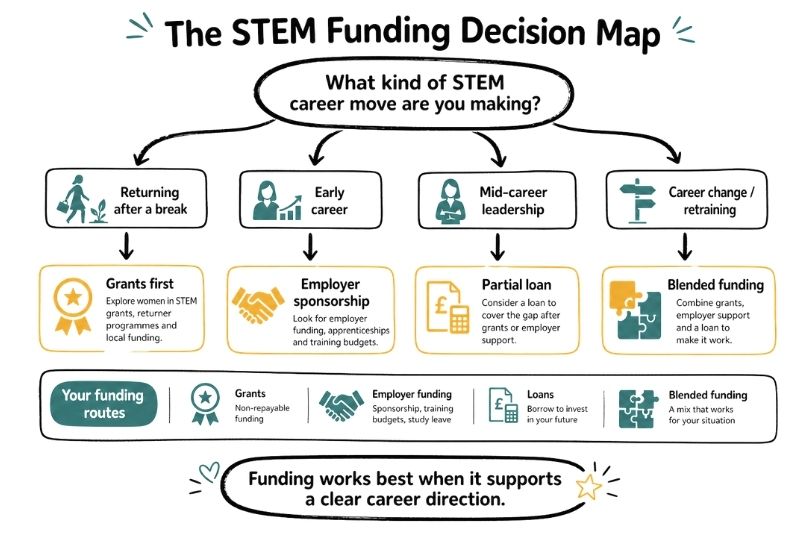

How to Choose the Right Funding Path for Your STEM Career

Choosing between funding options gets easier when you stop thinking in product categories and start thinking in career situations.

A woman returning after a break doesn’t need the same answer as an early-career analyst or a mid-career engineer aiming for leadership. The better question is, “What kind of career move am I funding?”

If you’re returning after a break

Your main challenge may not be academic ability. It may be timing, confidence, and cash flow.

In that situation, a smaller course with a direct line to employment often makes more sense than an expensive, broad qualification. Think in terms of relevance. What will convince a hiring manager that your skills are current?

Your decision checklist might look like this:

Choose shorter, employment-facing learning: certifications, technical refreshers, or provider-led vocational routes often work better than broad study with unclear outcomes.

Protect household cash flow: if childcare or reduced income is in the mix, avoid borrowing to the edge of your budget.

Value flexibility: a rigid repayment plan can become stressful if your return to work takes longer than hoped.

A grant-first, loan-second approach is often the safest fit here.

If you’re early in your STEM career

Early-career women usually face a different problem. The course may be useful, but your salary base is still developing.

That changes how a loan feels month to month. A manageable payment on paper can still be tight once rent, travel, software, and exam costs are real.

For this stage, ask yourself:

Question

Why it matters

Does the course unlock a specific role?

Borrowing is easier to justify when the role change is visible

Can your employer contribute anything?

Even partial help can reduce reliance on debt

Are you paying for prestige or practical skill?

Employers often reward applied capability more than course branding

Will the qualification still matter in a year or two?

Fast-moving technical areas can make some training date quickly

If you’re aiming for leadership mid-career

For mid-career women, the maths changes again. The course cost may be higher, but the upside can also be more strategic.

Mid-career women in STEM aged 35 to 50 earn 17% less than male peers, and loan-funded leadership programmes can yield a 2.5x ROI via promotions, yet only 8% of private loan schemes actively target STEM pay equity according to this PMC-hosted source cited in the brief. That doesn’t mean every leadership course is worth borrowing for. It does mean leadership funding deserves serious consideration when the programme connects to a real advancement pathway.

At this stage, women often underspend on themselves. They’ll finance technical study but hesitate over management or executive development, even when the next pay step depends on leadership credentials, strategic exposure, or sponsor-backed visibility.

The best leadership funding choice isn’t the cheapest course. It’s the programme that your sector and target employer will actually recognise.

Loan or grant

This question comes up constantly, and the answer depends on urgency.

Wait for a grant when the timeline is flexible and the opportunity is still likely to be there later. Use a loan when delaying the qualification would block your return, promotion, or entry into a live hiring cycle.

A simple way to test the decision is to write two short statements:

“If I wait, I gain…”

“If I wait, I risk…”

That usually brings clarity fast.

One decision many women skip

Ask whether the qualification itself creates visibility, not just skill.

Some programmes include mentor access, employer projects, alumni communities, or recognised status in your field. Those features can matter as much as content, especially if you’ve been overlooked before.

Recognition can also come through awards, applications, and profile-building activity that sits alongside formal study. If you’re building momentum for progression, it’s worth looking at awards for women in STEM as part of the wider career strategy.

The right funding path supports more than a course. It supports the version of your career you’re trying to build next.

A Step-by-Step Guide to Your Funding Application

Applications feel draining when they mix life admin, financial language, and deadlines. The easiest way through is to treat the process like a technical project. Break it into parts. Don’t rely on memory.

Step 1 Gather your evidence early

Most lenders, employers, and grant bodies want some version of the same core documents.

Create one folder and collect:

Identity documents: passport, driving licence, or other accepted ID

Proof of address: recent utility bill, bank statement, or official letter

Course details: offer letter, provider invoice, syllabus, and dates

Financial records: payslips, bank statements, or tax documents if requested

Career evidence: CV, LinkedIn profile, or a short statement about why the course supports employability

If you’re returning after a break, add a short written summary of your career history. It can help you answer application questions consistently.

Step 2 Build a real budget

At this point, many people underprepare. They budget for fees and forget the surrounding costs.

Use a simple layout like this:

Budget item

Estimated cost

Tuition or course fees

Exam or assessment fees

Software, books, or equipment

Travel or commuting

Childcare or caring cover

Lost earnings or reduced hours

Emergency buffer

The point isn’t perfection. The point is honesty.

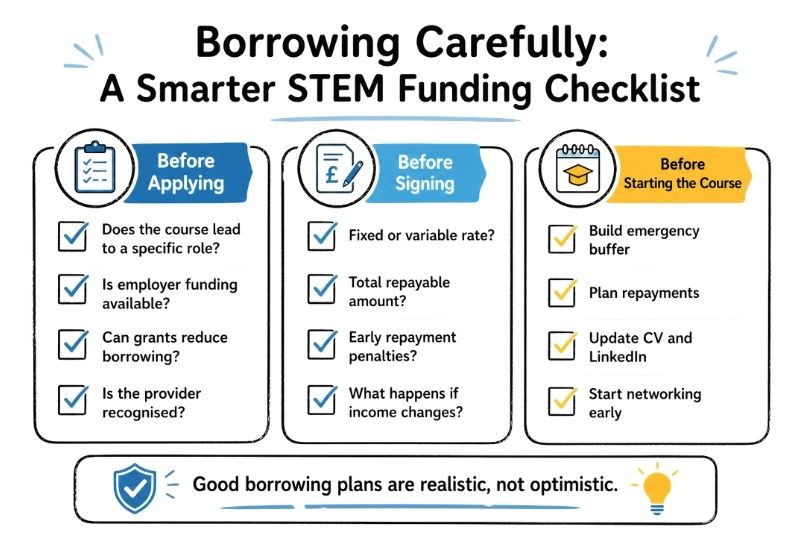

Step 3 Match the funding to the course

Before you apply, check the practical fit.

Some funding only works for approved providers. Some lenders prefer vocational training over general study. Some employers only fund training tied to current job duties.

If your course doesn’t fit the funding rules, a polished application won’t save it.

Step 4 Prepare for the credit and affordability questions

Private lenders may ask whether you can repay the loan based on your current circumstances, not your hoped-for future salary.

Be ready to explain:

your present income

regular household commitments

why the course improves employability

how you’ll manage repayments if income changes

Keep those answers plain and factual. Don’t overstate. Don’t hide constraints.

Step 5 Write a short funding case

Even when a full personal statement isn’t required, it helps to draft one for yourself.

Include:

Your goal: the role, specialism, or progression step you’re targeting

Why this course: what it teaches that is directly relevant

Why now: the reason timing matters

How you’ll manage the plan: work pattern, study time, and repayment thinking

A written version keeps your applications consistent.

For a useful framework to organise this thinking, use a structured career development plan. It helps turn “I want to upskill” into a more credible funding story.

Step 6 Review before submitting

Leave one day between finishing and submitting if you can.

Check:

Names and dates

Provider details

Loan or grant amount requested

Repayment terms

Attachments and uploads

Small admin errors can slow an otherwise strong application. Accuracy is part of affordability because delays can affect enrolment and payment timing.

A calm, well-organised application won’t guarantee approval. It does give you a clearer, stronger case.

Managing Repayment and Mitigating Financial Risk

You finish the course, the invoice is paid, and the main test begins a few weeks later. A repayment leaves your account on the same day as rent, childcare, or travel costs. For many women in STEM, especially returners and mid-career professionals, the risk is not only the loan itself. It is the timing mismatch between paying for training now and seeing the career benefit later.

Repayment works best when you treat it like a systems problem. Engineers do this all the time. You do not test only for ideal conditions. You plan for delays, weak points, and backup options.

Choose repayment terms for stability, not just a lower monthly figure

A lower monthly payment can help cash flow, but it can also keep you in debt for longer and increase the total amount repaid. The practical question is simpler than it sounds. Which option still looks manageable if your next role takes longer to secure, your hours change, or an unexpected cost lands at the wrong time?

If you are comparing offers, focus on three points:

Monthly repayment: what leaves your account each month

Total repayable: what the borrowing costs overall

Early repayment rules: whether you can reduce interest by paying extra without fees

That last point matters more than many applicants expect. If a bonus, pay rise, or employer contribution arrives later, flexible overpayments can shorten the life of the debt.

Fixed and variable rates, in plain English

A fixed rate gives you the same repayment structure for the agreed period. That makes planning easier.

A variable rate can rise or fall. If your budget already has very little spare room, that uncertainty can create pressure fast. Women returning after a career break often need predictability more than the small possibility of a lower rate later.

Neither option is automatically right. Match the rate type to your real life, not to the most optimistic version of the next 12 months.

Build your repayment plan before your course starts

A course budget and a repayment budget are not the same thing.

Write out a simple plan on one page. Include your take-home income, fixed household costs, the month repayments begin, and what happens if your career move is delayed. If you are stacking funding from more than one source, such as a smaller loan plus employer support and a grant, map the payment dates clearly so you are not covering gaps on a credit card.

A useful stress test is this: could you still make the payment for three months if nothing changed as quickly as you hoped?

Use these headings:

Base income: your current reliable income, not projected salary after the course

Course-related costs that continue: software, travel, membership fees, exam resits

Fallback actions: what you would pause, reduce, or renegotiate first

Overpayment plan: when you would pay extra, and under what conditions

If leadership training is part of your next step, compare the likely payoff as carefully as the cost. Programmes such as ILM Level 5 leadership development for women in STEM are strongest when they sit inside a wider progression plan rather than being funded on hope alone.

What to do early if repayment starts to look difficult

Silence usually gives the problem more time to grow.

If your job move, contract renewal, or return to full-time work is slower than expected, contact the lender before you miss a payment. Explain the change clearly. Ask what formal support or revised arrangements exist. Keep notes of dates, names, and what was agreed.

This matters for returners in particular. A gap on your CV does not mean weak prospects, but it can mean a slower hiring process while you rebuild networks, update technical confidence, or re-enter a changed sector.

Risk reduction strategies that help in real life

The goal is not to remove all risk. It is to keep one setback from turning into several.

Borrow only for the shortfall: if sponsorship, savings, or a niche grant can cover part of the cost, reduce the loan size.

Keep a small buffer untouched: even a modest emergency fund can stop one bad month becoming missed payments.

Avoid stacking expensive credit on top: using cards or buy-now-pay-later for living costs during study can make repayment much harder.

Link the course to action now: update your CV, restart your network, and apply for roles while you study.

Check whether your employer will reimburse later: some firms will not fund study upfront but will contribute after completion or promotion.

Review the return in role terms, not only salary terms: a course that leads to more secure work, better flexibility, or a credible route back into STEM may still be worth it, but only if the borrowing remains affordable under your current conditions.

Good borrowing plans are rarely dramatic. They are quiet, realistic, and well tested. That approach gives you more room to use funding as a tool for career progress, rather than carrying a repayment burden that limits your next move.

Investing in Your Future as a Leader in STEM

A well-chosen course can change your career direction, strengthen your earning power, and help you step back into STEM with more confidence. A poorly chosen loan can do the opposite. That’s why the decision needs both ambition and caution.

The strongest mindset is to treat funding as a tool, not a rescue plan. Use grants where you can. Ask employers first. Borrow carefully. Then measure the course against the role, pay progression, and visibility it can create.

And if leadership is your next move, practical development options like ILM Level 5 can be part of a larger plan to move from technical excellence into recognised influence.

Your future in STEM is worth funding carefully.

Frequently Asked Questions for Women in STEM

Can I use career development loans for a course after a career break

Sometimes, yes. The key question is whether the lender or funding body sees the course as employability-focused and whether you can meet their eligibility checks.

If you’ve been out of work, strengthen your application with a clear explanation of the role you’re targeting and why the course supports a return to work.

Should I wait for a grant instead of taking a loan

Wait if the course can be delayed without harming your career momentum. Don’t wait if the delay means missing a live hiring window, a returnship opportunity, or a promotion pathway.

A grant is cheaper. Timing still matters.

What if I need funding for childcare as well as tuition

Build childcare into your total budget from the start. Don’t treat it as a side issue.

For many women, childcare is part of the cost of training, not a separate personal expense. If a funding product won’t cover it directly, try to offset that gap with savings, family support, employer flexibility, or grant funding elsewhere in your plan.

Are private career development loans always a bad idea

No. They can be useful when the training is tightly linked to employability and other support isn’t enough.

They become risky when the course outcome is vague, the repayment terms are unclear, or you borrow more than your budget can safely carry.

What if my employer offers partial support only

Take it seriously. Partial support can still make a loan much safer.

You might ask the employer to cover exam fees, one module, study leave, or a direct contribution tied to course completion. Even limited help can reduce the amount you need to borrow.

How do I know if a course is worth funding

Use three tests:

Role test: does it help you reach a specific next job

Recognition test: will employers in your field value it

Repayment test: can you still manage if outcomes take longer than expected

If a course fails two of those three tests, pause before borrowing.

Written by The Women In Stem Network

The Women in STEM Network is a global professional community supporting women across science, technology, engineering, and mathematics.

We bring together networking, mentoring, training, live events, and career opportunities in one place, helping women at every stage of their STEM journey to thrive, progress, and lead.

Built by experts with decades of experience in STEM, WiSN exists to strengthen careers, expand opportunity, and help organisations access and retain outstanding talent.

Our members include students, early-career professionals, senior leaders, and career returners from around the world.

If you would like to go further, consider joining the Women in STEM Network. Membership gives you full access to our mentoring programmes, on demand training, live events, forums, and global networking opportunities. We are a rapidly growing platform and warmly welcome visitors and new members at every career stage. Concessionary rates are available for those on low incomes and for members based in developing countries. Membership fees directly support the growth of the platform and help us build better, more accessible resources for women in STEM.

Discover the future of STEM in India with our essential guide Explore opportunities, government initiatives, career prospects and practical steps for success

Explore How The Confidence Gap Women Face In Stem Affects Careers And Learn Practical Strategies To Build Confidence And Achieve Greater Equity In Science

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.